Why an Emergency Fund Is More Important Than Ever in 2025

If 2020 taught us anything, it’s that life is unpredictable. Job losses, medical bills, car repairs, or even global crises can disrupt your finances overnight. That’s why having an emergency fund is one of the most important steps in personal finance.

In 2025, the stakes are even higher:

- Inflation continues to drive up the cost of essentials, such as rent and groceries.

- Credit card APRs remain above 20% on average, according to NerdWallet’s 2025 report. Falling back on debt during a crisis only exacerbates the situation.

- Unexpected expenses are more common than most people realize — Bankrate’s 2025 emergency savings report found that only 46% of Americans could cover a $1,000 emergency from savings, while 24% have none at all.

👉 The solution? Build a financial safety net that gives you peace of mind and keeps you from going into debt when the unexpected happens. That safety net is your emergency fund.

What Is an Emergency Fund?

An emergency fund is a dedicated pool of cash set aside for unexpected, essential expenses. Think:

- Medical emergencies

- Car or home repairs

- Job loss or reduced hours

- Travel for family emergencies

It is not for vacations, impulse shopping, or routine bills. Those belong in your regular budget. (See our guide: How to Create a Budget That Actually Works in 2025).

💡 Think of your emergency fund as an insurance policy you create for yourself — it doesn’t grow fast, but it protects you from financial disaster.

Why You Need an Emergency Fund in 2025

If you’ve ever had a flat tire, a surprise medical bill, or an unexpected job loss, you know how quickly life can derail your finances. That’s why an emergency fund is the foundation of financial security.

1. Inflation and Rising Costs

In 2025, prices of everyday essentials like rent, groceries, and healthcare will remain elevated due to ongoing inflation. Even a small emergency can now cost hundreds of dollars more than it did just a few years ago. Without savings, many people turn to credit cards or loans, which come with APR rates over 20%, according to NerdWallet’s 2025 credit card report.

2. Job Market Uncertainty

While unemployment remains relatively stable, layoffs and income cuts still happen — especially in industries facing automation or restructuring. Without a safety net, losing even one paycheck can push families into debt.

3. Americans Are Underprepared

Bankrate’s 2025 emergency savings report revealed:

- Only 46% of U.S. adults have enough saved to cover three months of expenses.

- 24% have no emergency savings at all.

- 37% had to dip into savings in the past year.

This means more than half of households are just one unexpected bill away from financial stress.

4. Emergencies Are Guaranteed — Not Optional

According to a Federal Reserve survey, 56% of U.S. adults experienced an unexpected large expense in the last year. Emergencies are not “if” but “when.” An emergency fund makes the difference between paying cash vs. spiraling into debt.

Takeaway: An emergency fund isn’t about fear — it’s about freedom. When you know you can handle life’s surprises, you stress less and stay on track toward long-term goals like saving and investing.

How Much Should You Save in Your Emergency Fund?

One of the biggest questions beginners ask is: “How much should I actually keep in my emergency fund?” The answer depends on your income stability, lifestyle, and personal risk tolerance.

1. Starter Emergency Fund (1 Month of Expenses)

If you’re just starting, aim for one month’s worth of essential expenses (rent, food, utilities, transportation).

- Why: It’s achievable quickly and gives you immediate protection against small emergencies.

- Example: If your essential monthly expenses are $2,000, start with a $2,000 target.

2. Standard Emergency Fund (3–6 Months of Expenses)

Most financial experts, including Bankrate and CFPB, recommend an emergency fund of 3–6 months of living expenses.

- Why: This covers job loss, medical bills, or bigger unexpected costs.

- Example: If your household spends $3,000/month, aim for $9,000–$18,000.

3. Extended Emergency Fund (9–12 Months of Expenses)

For freelancers, gig workers, or people with irregular income, a larger safety net is wise.

- Why: Income can be unpredictable, and it may take longer to find new work if you lose a client or contract.

- Example: If you’re self-employed and spend $4,000/month, your target could be $36,000–$48,000.

4. Rule of Thumb Approach

- Stable job, dual-income household → 3 months may be enough.

- Single-income household → Aim for 6 months.

- Freelancers/self-employed → Aim for 9–12 months.

👉 Pro Tip: Use a calculator (like NerdWallet’s Emergency Fund Calculator) to estimate your personal target.

✅ Takeaway: The “right” emergency fund isn’t the same for everyone. Start small, then build until you reach the amount that lets you sleep peacefully at night.

Where to Keep Your Emergency Fund

Once you know how much to save, the next step is deciding where to keep your emergency fund. The goal is to balance safety, liquidity, and a bit of interest — so your money is easy to access but still earning something.

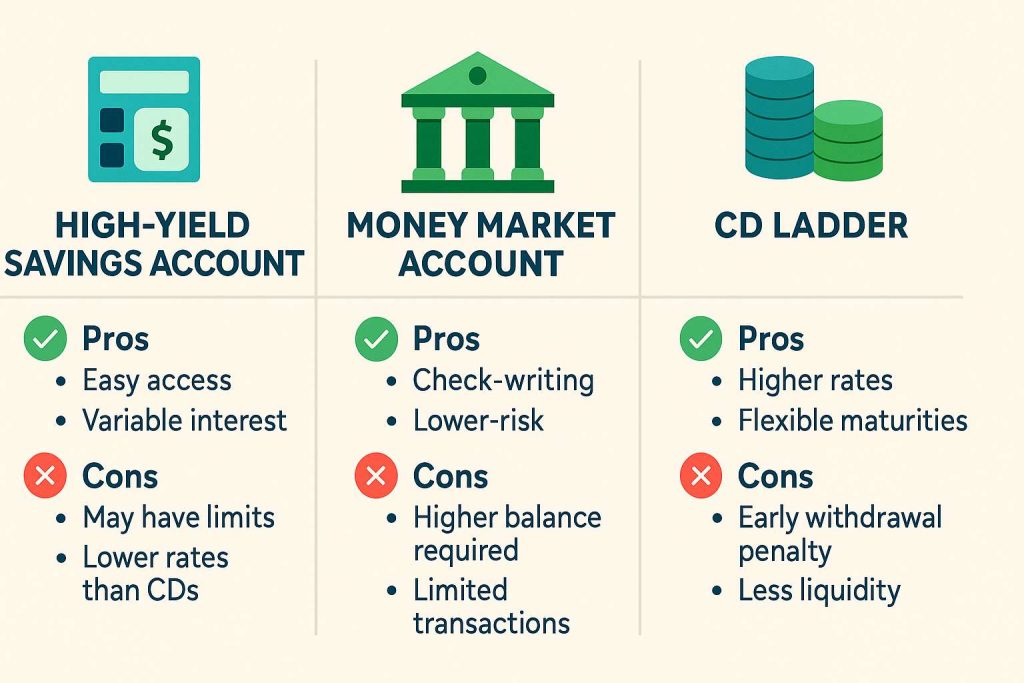

1. High-Yield Savings Accounts (HYSA)

- Best for: Most people.

- Why: FDIC-insured, instantly accessible, and interest rates are much higher than traditional savings accounts.

- 2025 Example: Many HYSAs pay 4%+ APY, according to Bankrate.

- Pro Tip: Open your HYSA at a different bank from your checking to reduce temptation, but still keep it accessible in 1–2 business days.

2. Money Market Accounts (MMA)

- Best for: Those who want check-writing or debit access.

- Why: Similar to HYSAs, but often come with limited transactions.

- Interest: Comparable to HYSAs, depending on the bank.

- Downside: May require higher minimum balances.

3. Certificates of Deposit (CDs)

- Best for: Advanced savers who want higher interest on a portion of their fund.

- Why: Locking in a CD for 6–12 months may earn slightly higher rates.

- Downside: Not as liquid — you’ll pay a penalty if you withdraw early.

- Pro Tip: Use a CD ladder (staggered maturities) if you want higher yields while keeping some liquidity.

4. Cash (Only a Small Portion)

- Best for: Quick access to small emergencies.

- Why: A few hundred dollars in cash at home can cover urgent needs (like if ATMs go down).

- Downside: No interest, and risky to keep too much cash on hand.

5. Where Not to Keep Your Emergency Fund

- Stocks, Crypto, or REITs: Too volatile — your $5,000 could drop to $3,000 right when you need it.

- Retirement Accounts (401k, IRA): Withdrawals come with taxes and penalties.

✅ Takeaway: The best home for your emergency fund is a high-yield savings account (HYSA) — safe, liquid, and earning interest. Money markets or CDs can be good secondary options, but avoid risky assets.

Step-by-Step: How to Build an Emergency Fund Fast

Building an emergency fund can feel overwhelming, but the secret is breaking it down into small, repeatable steps. Here’s a simple plan to grow yours — even if you’re starting from zero.

Step 1: Set a Clear Target

- Decide your goal: starter ($1,000), 3 months, 6 months, or 12 months of expenses.

- Write the number down — specific goals are easier to reach.

Step 2: Automate Your Savings

- Set up automatic transfers from checking to your emergency fund every payday.

- Even $50/week adds up to $2,600 a year.

- Pro Tip: Treat savings like a bill you must pay.

Step 3: Cut Small Expenses That Don’t Hurt

- Review subscriptions — cancel unused ones.

- Cook at home 2–3 nights a week.

- Buy generic brands instead of name brands.

👉 For more strategies, see our guide: 25 Practical Ways to Save Money Every Month.

Step 4: Use Windfalls Wisely

- Tax refund? Work bonus? Unexpected gift?

- Put at least 50% into your emergency fund before spending the rest.

- One lump-sum boost can cut months off your savings timeline.

Step 5: Start a Small Side Hustle

- Freelancing, tutoring, delivery apps, or selling unused items.

- Even $200 extra per month = $2,400/year into your emergency fund.

- Bonus: Once your fund is full, you can redirect that money into investing.

Step 6: Track Your Progress

- Use a visual tracker or spreadsheet.

- Celebrating milestones (first $500, then $1,000, etc.) keeps you motivated.

✅ Takeaway: The fastest way to build an emergency fund is a mix of automation + lifestyle tweaks + extra income. Start small, stay consistent, and use windfalls to accelerate your progress.

Emergency Fund vs Regular Savings

Many beginners ask: “Isn’t my savings account already an emergency fund?” The short answer: not exactly. While both involve saving money, they serve very different purposes.

1. Purpose

- Emergency Fund: Strictly for unexpected, essential expenses (job loss, medical bills, car repair).

- Regular Savings: For planned goals like vacations, new gadgets, down payments, or education.

2. Accessibility

- Emergency Fund: Should be kept separate (preferably in a HYSA or money market account) so you’re not tempted to dip into it.

- Regular Savings: Can stay in your main bank savings account since it’s for planned spending.

3. Mental Separation

Keeping your emergency fund separate prevents accidental spending. Label your accounts clearly, for example:

- “Emergency Fund — Do Not Touch”

- “Travel Savings 2025”

👉 This small psychological trick makes it much easier to stick to your goals.

4. Returns vs Safety

- Emergency Fund: Prioritizes safety and liquidity, not high returns.

- Regular Savings: Can sometimes be placed in slightly riskier assets (CDs, short-term bonds) if you don’t need the money right away.

✅ Takeaway: Your emergency fund is your financial shield. Your regular savings are your financial growth bucket. You need both to stay prepared and enjoy life.

Common Emergency Fund Mistakes to Avoid

- Keeping it in your checking account → Too tempting to spend.

- Investing it in stocks or crypto → Too risky, you could lose money right when you need it.

- Mixing it with regular savings → Harder to track progress and discipline.

- Not starting at all because the goal feels too big → Even $500 is better than $0.

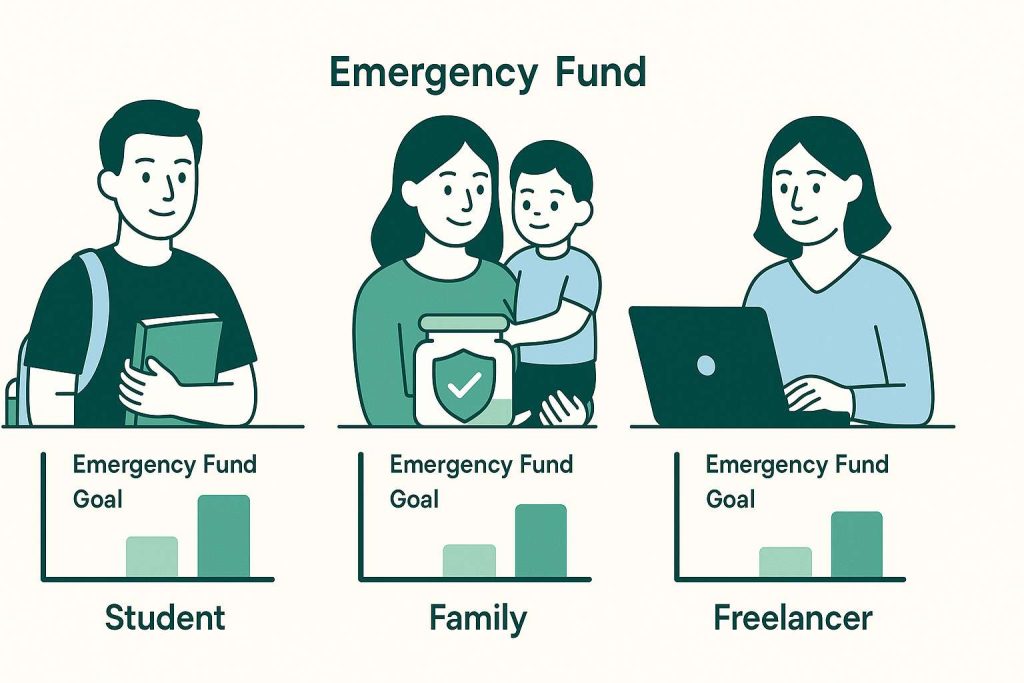

Case Study Scenarios: Emergency Fund in Action

Sometimes numbers make it real. Here’s what an emergency fund looks like for different people:

1. College Student (Income: $1,200/month)

- Expenses: $600 housing, $200 food, $150 transport, $100 misc.

- Goal: $1,000 starter emergency fund.

- Plan: Save $100/month → reach goal in 10 months.

👉 Why it works: Covers car repair, laptop replacement, or medical copay without using credit cards.

2. Family of Four (Income: $5,000/month)

- Expenses: $1,500 housing, $800 food, $500 transport, $400 insurance, $1,200 misc.

- Goal: $15,000 (3 months of expenses).

- Plan: Automate $500/month + apply tax refund → goal in ~2 years.

👉 Why it works: Protects against job loss, medical bills, or large home repairs.

3. Freelancer (Income: $3,500/month irregular)

- Expenses: $2,500 essential bills.

- Goal: $25,000 (9–12 months).

- Plan: Save $400/month + 50% of large project payments.

👉 Why it works: Freelancers face inconsistent income — larger buffers provide stability.

FAQs on Emergency Funds

1. How much should I keep in an emergency fund?

At least 3–6 months of essential expenses. Freelancers or single-income households should aim for 9–12 months.

2. Where is the best place to keep an emergency fund?

In a high-yield savings account (HYSA) or money market account, safe, liquid, and earn interest.

3. Can I use credit cards instead of an emergency fund?

Not a good idea — average APR is 20%+. Using debt for emergencies often makes problems worse.

4. Should I invest my emergency fund?

No. Stocks and crypto are too volatile. Your emergency fund should always be safe and accessible.

5. What if I can’t save much right now?

Start small. Even $10–$20/week builds momentum. A $500 buffer already prevents most small emergencies from turning into debt.

6. Do I still need an emergency fund if I have insurance?

Yes. Insurance doesn’t cover everything (deductibles, lost income, unexpected bills). Your emergency fund fills those gaps.

Conclusion: Secure Your Future with an Emergency Fund

An emergency fund isn’t about being pessimistic — it’s about being prepared. In 2025, with rising costs, unpredictable job markets, and high-interest debt, having savings for the unexpected is no longer optional.

Here’s your step-by-step action plan:

- Set a target (start with $1,000, then grow to 3–6 months).

- Choose the right place (HYSA or money market).

- Automate savings every month.

- Boost with windfalls and side hustles.

- Keep it separate from regular savings to avoid temptation.

👉 Ready to get started?

- Read our guide: How to Create a Budget That Actually Works in 2025

- Discover 25 Practical Ways to Save Money Every Month

- Download our Free Interactive Budget Template to track and grow your emergency fund today.

The peace of mind you’ll gain is priceless — and your future self will thank you.