Why start investing in 2025 (and what it really means)

If you’re searching for investing for beginners advice, here’s the simplest truth: investing is how your money starts working for you. Savings protect purchasing power for short-term needs, but long-term growth typically comes from owning productive assets (stocks, bonds, funds, real estate via REITs). The U.S. SEC’s investor education hub explains the core investment products and why most people reach financial security by saving and investing over time, not by chance.

Understanding the basics of Investing for Beginners will help you make informed decisions.

Investing for Beginners is an important step to building wealth over time.

Investing for Beginners involves knowing key strategies to grow your wealth.

At the same time, inflation slowly erodes cash. The Consumer Price Index (CPI) measures those price changes and why “do nothing” with idle cash can lose buying power over time.

So your beginner goal isn’t to “beat the market” next month—it’s to build a simple, low-cost, diversified plan you can stick to for years. Regulator and industry resources emphasize the same pillars: set goals, diversify, mind costs, automate contributions, and avoid fraud.

Why many beginners struggle (so you don’t)

Before buying anything, understand the traps that make new investors quit:

- No financial foundation. Investing before building an emergency fund or a basic budget forces you to sell at the worst times.

- Chasing hype instead of a plan. Sensational tips, hot stocks/coins, FOMO. The SEC’s education pages stress having goals, understanding risks, and recognizing red flags.

- Zero diversification. A single stock (or narrow theme) = concentrated risk. Regulators spell out why asset allocation + diversification + periodic rebalancing are essential risk tools. FINRAInvestor

- Ignoring costs & behavior. High fees and over-trading quietly drain returns; panic selling locks in losses.

- Misusing dollar-cost averaging (DCA). DCA can help behaviorally (reduces regret/volatility of entry), but research shows lump-sum often has higher expected returns—know the trade-off and choose the method you’ll actually follow.

For those starting out, Investing for Beginners means focusing on low-cost options.

Takeaway: Your edge as a beginner isn’t secret picks—it’s a simple, diversified, low-cost process you’ll keep contributing to through different markets (and that starts with a cash buffer + budget).

Ground rules for this guide (what we’ll cover next)

- Step 1 — Build your foundation: emergency fund, debt priorities, contribution target

- Step 2 — Know what you’re buying: stocks, bonds, index funds/ETFs, REITs, and cash-like instruments—what they are, why they’re used, and where they fit.

- Step 3 — Pick beginner-friendly wrappers: broad index funds/ETFs and how to choose (fees, index, tracking).

- Step 4 — Automate & allocate: basic asset allocation, rebalancing, and contribution automation. FINRA

- Step 5 — Avoid common mistakes: hype chasing, fee traps, lack of diversification, and tax-cost surprises.

Compliance note: Nothing here is personal financial advice. Use these sources to learn and tailor to your situation; consult a licensed advisor if needed.

Step 1: Build Your Financial Foundation Before You Invest

The first step in investing for beginners is not opening a brokerage account or picking stocks. It’s making sure your financial foundation is strong. Without this, you’ll be forced to sell investments when life throws surprises, which is one of the fastest ways to lose money.

1. Build an Emergency Fund

Before investing, set aside at least 3–6 months of essential expenses in a savings account.

- Why? Because markets are unpredictable. If your car breaks down or you lose your job, you don’t want to sell investments at a loss.

- According to Bankrate’s 2025 emergency savings report, only 46% of Americans have enough savings to cover three months of expenses, while 24% have none.

- Keep this fund in a high-yield savings account (HYSA) or money market account for safety and liquidity.

2. Pay Down High-Interest Debt

If you’re carrying credit card balances at 20% APR, investing won’t help — your debt is eating wealth faster than most investments can grow.

- Example: Paying off a $5,000 balance at 20% APR is like earning a guaranteed 20% return.

- NerdWallet’s 2025 credit card report shows the national average APR is over 20%, making debt repayment the best “investment” many beginners can make.

3. Create a Budget That Supports Investing

Investing for Beginners is about establishing a solid financial foundation first.

You need to know how much you can invest each month. That comes from building a realistic budget.

- A budget ensures you’re not investing money you’ll need next week for rent or groceries.

- How to Create a Budget That Actually Works in 2025.

- 25 Practical Ways to Save Money Every Month for extra cash flow ideas.

4. Decide Your Investment Contribution Target

Once your emergency fund and debt are under control, decide how much to invest.

- Rule of thumb: 10–20% of your income.

- Start smaller if needed — even $50/month grows through compound interest.

- Example: $50/month invested in a low-cost S&P 500 ETF (assuming ~7% annual returns) can grow to $12,000+ in 15 years.

Takeaway: Investing only works if you don’t need to pull money out too soon. The foundation — emergency fund + debt control + budget + contribution target — ensures you can stay invested long enough to benefit from compounding.

Investing for Beginners often starts with creating an emergency fund.

For Investing for Beginners, paying down high-interest debt is crucial.

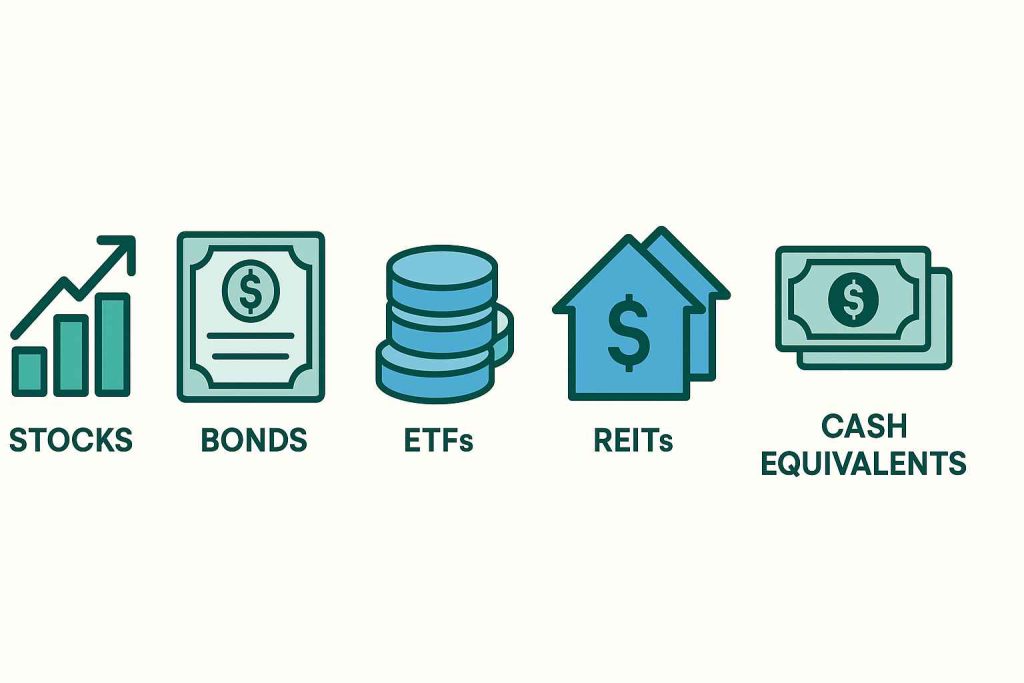

Step 2: Understand Key Investment Types

If you’re new to investing for beginners, the alphabet soup of terms—stocks, ETFs, bonds, REITs—can feel intimidating. But every investment you’ll encounter fits into just a few categories. Understanding these helps you make confident choices.

1. Stocks (Equities)

- What they are: Ownership shares of a company. When you buy stock, you own a piece of that business.

- Why beginners use them: Over the long term, stocks historically deliver the highest returns compared to other asset classes.

- Risks: Prices fluctuate daily. Short-term losses are common, but historically, U.S. stocks have returned ~10% annually before inflation.

- Beginner tip: Instead of buying individual stocks, most experts recommend starting with diversified stock funds (ETFs or mutual funds).

2. Bonds (Fixed Income)

- What they are: Essentially a loan you give to a company or government, which pays you interest.

- Why beginners use them: Bonds are generally less volatile than stocks and provide steady income.

- Risks: Inflation can eat away at returns, and bond prices fall when interest rates rise.

- Example: U.S. Treasury bonds are considered among the safest investments in the world.

Creating a budget is essential for Investing for Beginners to know how much to invest.

Investing for Beginners requires clarity on your investment goals.

3. Exchange-Traded Funds (ETFs) & Index Funds

- What they are: “Baskets” of stocks or bonds that you buy as a single investment. They track an index like the S&P 500.

- Why beginners use them:

- Diversification (hundreds of stocks in one fund).

- Low fees (many charge under 0.10%).

- Easy to buy through any brokerage.

- Example: Vanguard’s S&P 500 ETF (VOO) gives instant exposure to 500 leading U.S. companies.

- Expert opinion: Morningstar emphasizes ETFs as the simplest way for beginners to access diversified portfolios.

4. Real Estate Investment Trusts (REITs)

- What they are: Companies that own and manage real estate, like apartments, shopping centers, or office buildings.

- Why beginners use them: REITs allow you to invest in real estate without buying property. They also pay dividends regularly.

- Risks: Can be sensitive to interest rates and economic cycles.

- Note: REIT ETFs give diversification across many types of properties.

5. Cash Equivalents (Safe Parking)

- What they are: Money market accounts, CDs (certificates of deposit), and Treasury bills.

- Why beginners use them: Safe place to park short-term money while earning more interest than a checking account.

- Example: As of 2025, many high-yield savings accounts (HYSAs) pay 4%+ interest, according to Bankrate.

- Best use: Emergency fund or short-term savings—not long-term investing.

Quick Comparison Table: Investment Types for Beginners

| Asset Type | Return Potential | Risk Level | Best For | Example Product |

|---|---|---|---|---|

| Stocks | High (7–10% long term) | High | Long-term growth | Apple stock, S&P 500 ETF |

| Bonds | Moderate (2–5%) | Low–Moderate | Stability + income | U.S. Treasury bond |

| ETFs/Index Funds | Moderate–High | Moderate | Beginners seeking diversification | Vanguard S&P 500 ETF |

| REITs | Moderate | Moderate–High | Passive real estate exposure | VNQ (REIT ETF) |

| Cash Equivalents | Low (2–5%) | Very Low | Emergency funds, short-term needs | HYSA, Money Market Fund |

👉 Takeaway: Beginners don’t need to master every product. For most, a mix of ETFs (for growth) + some bonds (for stability) + cash for emergencies is the safest starting point.

Step 3: Pick Beginner-Friendly Platforms in 2025

Now that you know the types of investments, the next step in investing for beginners is choosing the right platform. The good news? In 2025, you don’t need a Wall Street broker. Anyone can start investing with as little as $1 on beginner-friendly apps and brokerages.

What to Look for in a Beginner Platform

When selecting a platform, keep these factors in mind:

- Low or No Commissions: Most major brokerages now offer commission-free trades.

- Fractional Shares: Lets you buy a piece of a stock or ETF (e.g., $10 worth of Amazon instead of one $3,000 share).

- Automation Features: Ability to set recurring investments (helps with dollar-cost averaging).

- Educational Tools: Built-in resources for beginners to learn as they invest.

- Strong Security: SIPC protection, 2FA, and regulatory oversight.

👉 Pro Tip: Avoid platforms that push day trading or speculative bets — they often lead beginners into bad habits.

Best Beginner Platforms in 2025

- Fidelity

- No commissions, zero account minimums.

- Offers fractional shares + strong research tools.

- Rated highly by NerdWallet.

- Vanguard

- Best for long-term investors focused on ETFs and index funds.

- Low-cost funds with strong historical performance.

- Great if you’re serious about retirement investing.

- Robinhood

- Simple, beginner-friendly interface.

- Commission-free trades + fractional shares.

- Downsides: Limited research tools, encourages trading more than long-term investing.

- Acorns

- Rounds up your purchases and invests spare change automatically.

- Great for absolute beginners who want investing “on autopilot.”

- Betterment (Robo-Advisor)

- Automated portfolios based on your goals and risk tolerance.

- Hands-off option for beginners who don’t want to pick funds.

Which Platform is Right for You?

- If you want hands-on learning → Fidelity or Vanguard.

- If you want automation → Betterment or Acorns.

- If you want ease of use → Robinhood (but use responsibly).

👉 Beginner Tip: Don’t overthink the platform. Pick one, start with a small amount, and focus on consistent contributions. You can always move accounts later.

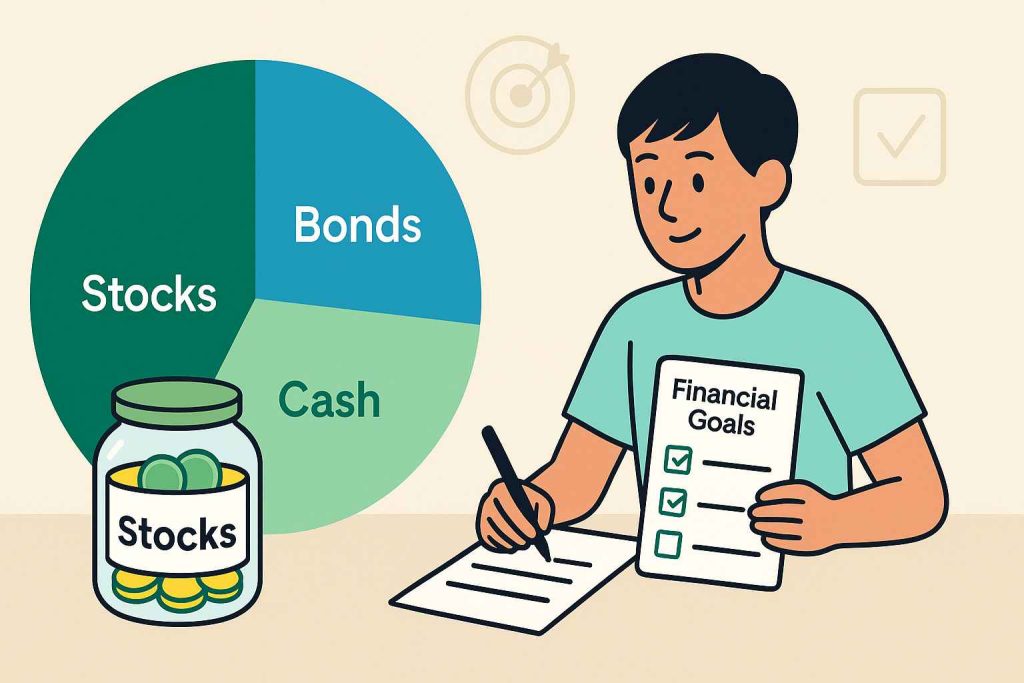

Step 4: Set Your Investment Goals & Asset Allocation

The heart of investing for beginners is making sure your money matches your goals. Before buying anything, ask: What am I investing for? The answer will shape your asset allocation — the mix of stocks, bonds, and other assets in your portfolio.

1. Define Your Goals

Your investments should serve a purpose. Examples:

- Short-Term (1–3 years): Buying a car, saving for a wedding → safer, cash-equivalents.

- Medium-Term (3–7 years): House down payment, grad school → mix of bonds + conservative ETFs.

- Long-Term (7+ years): Retirement, financial independence → mostly stocks/stock ETFs.

👉 The SEC recommends aligning investments with time horizon + risk tolerance.

2. Know Your Risk Tolerance

Risk tolerance = your ability to handle ups and downs.

- Conservative: More bonds, less stocks.

- Moderate: Balanced mix of stocks and bonds.

- Aggressive: Mostly stocks (long time horizon).

👉 Example: If you panic when your account drops 10%, you need a more conservative allocation.

3. Asset Allocation Basics

Asset allocation is how you spread money across categories (stocks, bonds, cash). It’s one of the biggest drivers of returns and risk.

Rule of Thumb:

- Young investors (20s–30s): 80–90% stocks, 10–20% bonds.

- Middle-aged (40s–50s): 60–70% stocks, 30–40% bonds.

- Retirement age: 40–50% stocks, 50–60% bonds/cash.

Investing for Beginners can be simplified through technology.

👉 For beginners, a simple “Target-Date Fund” or a 60/40 portfolio is often enough.

4. Dollar-Cost Averaging (DCA) vs Lump-Sum Investing

One key decision in investing for beginners is how to put money in.

- Dollar-Cost Averaging (DCA): Invest the same amount regularly (e.g., $200/month).

- Reduces timing risk.

- Good for beginners because it builds habit.

- Lump-Sum Investing: Put in all money at once. Historically gives better returns (because markets rise over time).

- Vanguard research found lump-sum beats DCA two-thirds of the time — but only if you can handle volatility.

Investing for Beginners shouldn’t be overwhelming with the right tools.

Finding the right platform is key for Investing for Beginners.

👉 Beginner takeaway: Start with DCA. Once you’re confident, lump-sum contributions can be used for windfalls (bonuses, tax refunds).

5. Automate Contributions

Automation is a beginner’s best friend:

- Set your brokerage or robo-advisor to pull money from checking monthly.

- You won’t forget, and you’ll avoid the temptation to “time the market.”

✅ Summary: Investing without goals is like flying without a destination. Define your time horizon, set an allocation you can live with, and use automation + DCA to stay consistent.

Step 5: Avoid Common Mistakes in Investing for Beginners

Even with the right plan, many new investors make avoidable mistakes that cost them money. If you understand these upfront, you’ll avoid the traps that derail most beginners.

1. Chasing “Hot” Stocks or Trends

- The mistake: Buying whatever is hyped on social media, YouTube, or news headlines.

- Why it hurts: By the time everyone is talking about it, the price is usually inflated — and you’re buying high.

- Example: Meme stocks like GameStop and AMC surged, but many beginners who bought late lost big.

- Fix: Stick with diversified ETFs and index funds instead of stock tips.

👉 The SEC warns that “get-rich-quick” investments are a common red flag for fraud and loss.

2. Overtrading

- The mistake: Buying and selling constantly, trying to “time the market.”

- Why it hurts: High fees, taxes, and emotional mistakes erode returns.

- Fix: Focus on long-term investing. Rebalance 1–2 times per year, not daily.

3. Ignoring Fees

- The mistake: Investing in funds with high expense ratios (1%+ annually).

- Why it hurts: A 1% fee can eat up $100,000+ of returns over 30 years on a $100,000 portfolio.

- Fix: Choose low-cost index funds (many under 0.10%). Vanguard and Fidelity lead the way with low fees.

4. Lack of Diversification

- The mistake: Putting all money into one stock, one sector, or one asset.

- Why it hurts: One bad company can wipe out your portfolio.

- Fix: Spread across asset classes (stocks + bonds), geographies (U.S. + international), and industries. ETFs make this easy.

👉 Diversification and periodic rebalancing are proven strategies regulators recommend to reduce risk.

5. Forgetting Taxes

- The mistake: Selling investments too quickly without considering taxes.

- Why it hurts: Short-term capital gains are taxed at regular income rates, often higher than long-term rates.

- Fix: Hold investments for at least a year when possible, and use tax-advantaged accounts (401(k), IRA). See IRS.gov for tax details.

6. Emotional Investing

- The mistake: Panic selling in downturns or getting greedy in bull markets.

- Why it hurts: Most investors underperform the market because of poor timing, not poor investments.

- Fix: Automate contributions and stick to your plan. Remember — downturns are opportunities to buy at lower prices.

✅ Beginner Takeaway: Avoiding mistakes is often more powerful than chasing returns. Slow, steady, diversified investing beats speculation 99% of the time.

FAQs on Investing for Beginners in 2025

1. How much money do I need to start investing in 2025?

You can start with as little as $1–$5 on platforms that offer fractional shares. Many robo-advisors also allow $10 minimums. The key is consistency, not the starting amount.

2. What’s the safest investment for beginners?

For absolute safety: high-yield savings accounts, money market funds, or U.S. Treasuries. For long-term growth, low-cost index funds are considered the best starting point for beginners by many financial experts.

3. Should I pay off debt before investing?

Yes — if it’s high-interest debt (like credit cards > 20% APR), pay that down first. It’s like earning a guaranteed 20% return. But you can invest small amounts while paying off lower-interest loans.

4. What’s the difference between stocks and ETFs?

- Stocks: Ownership in one company.

- ETFs: A basket of stocks or bonds (built-in diversification). Most beginners should start with ETFs or index funds.

5. Can I lose all my money investing?

If you buy a single stock, yes — companies can fail. But with a diversified ETF (like an S&P 500 fund), losing everything is virtually impossible unless the entire U.S. economy collapses.

6. What is dollar-cost averaging, and should I use it?

DCA means investing the same amount on a regular schedule (e.g., $200/month). It helps beginners avoid bad timing and emotional decisions.

7. Should beginners use a robo-advisor or DIY?

- Robo-advisors (like Betterment, Wealthfront) → Good if you want automated portfolios.

- DIY (Fidelity, Vanguard, Robinhood) → Good if you want to learn and manage yourself. Both are valid for beginners.

8. How do taxes affect beginner investing?

Short-term gains (<1 year) are taxed as ordinary income. Long-term gains are taxed at lower capital gains rates. Beginners should prioritize tax-advantaged accounts like 401(k)s and IRAs when possible.

9. Is investing risky for beginners in 2025?

Markets always carry risk, but the biggest risk for beginners is not investing at all. Inflation reduces the value of cash every year. A diversified portfolio reduces risk over time.

10. What’s the #1 rule for investing for beginners?

Start early, stay consistent, and don’t chase hype. Time in the market beats timing the market.

Start Your Investing Journey Today

Learning investing for beginners in 2025 doesn’t have to be overwhelming. Here’s the roadmap:

- Build your foundation → Emergency fund, pay off high-interest debt, create a budget.

- Understand investment types → Stocks, bonds, ETFs, REITs, cash.

- Pick a beginner-friendly platform → Fidelity, Vanguard, Acorns, Betterment.

- Set clear goals & asset allocation → Match investments to your time horizon and risk tolerance.

- Avoid mistakes → No hype chasing, minimize fees, diversify, and automate contributions.

👉 Next steps for you:

- Read How to Create a Budget That Actually Works in 2025 (Blog #1)

- Explore 25 Practical Ways to Save Money Every Month (Blog #2)

- Download our Free Interactive Budget Template to free up money for investing

It’s important for Investing for Beginners to set a realistic asset allocation.

The truth is, the best time to start investing was yesterday. The second-best time is today. Even small amounts, invested consistently, can grow into life-changing wealth thanks to compound interest.

Stay consistent. Stay patient. Your future self will thank you.